Beyond the Skyline: 5 Trends Redefining Philippine Real Estate in 2026

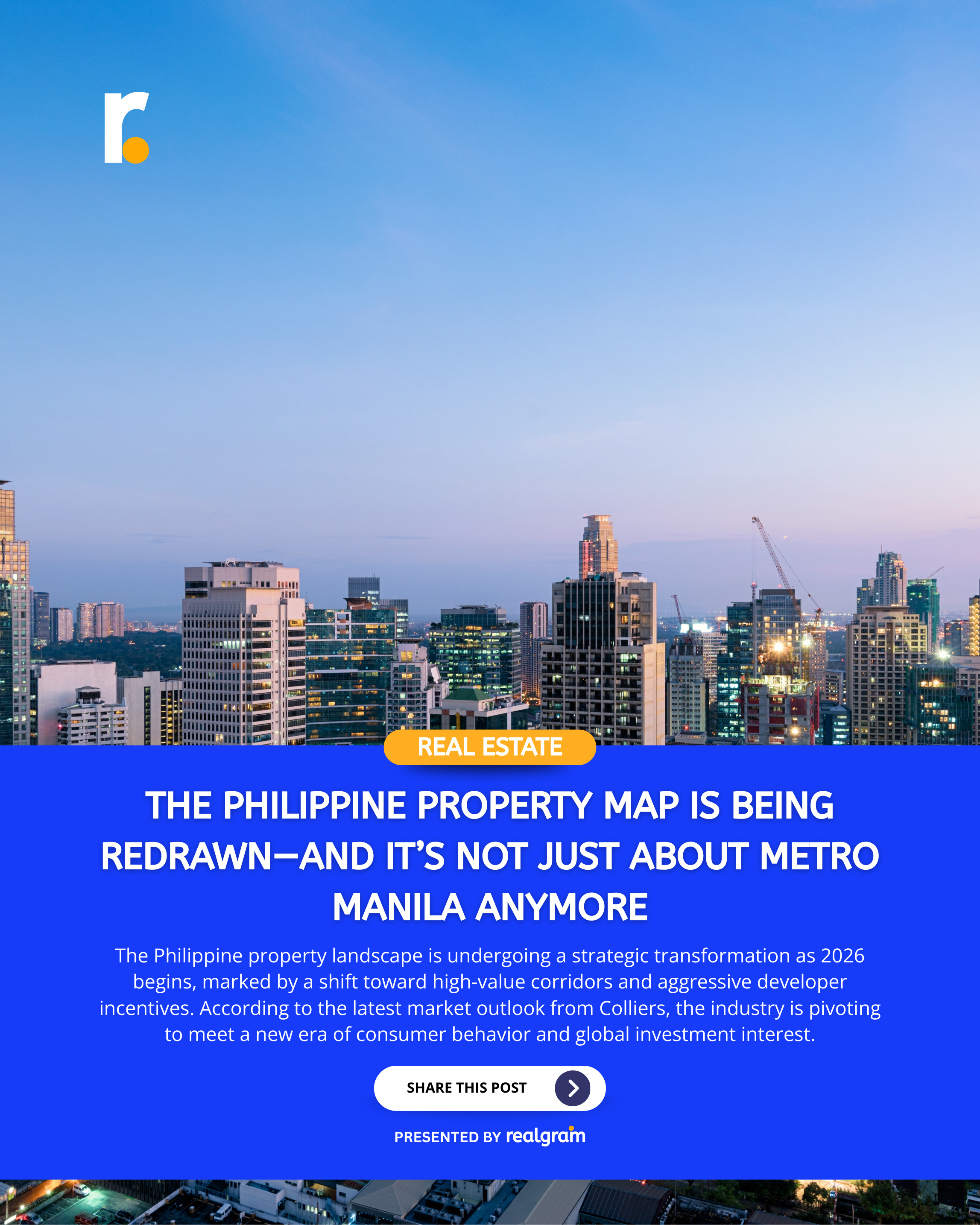

MANILA, Philippines — The Philippine property landscape is undergoing a strategic transformation as 2026 begins, marked by a shift toward high-value corridors and aggressive developer incentives. According to the latest market outlook from Colliers, the industry is pivoting to meet a new era of consumer behavior and global investment interest.

Joey Bondoc, Director for Research at Colliers, identifies five critical sectors that are set to define the market this year. From the high-rise hubs of Metro Manila to the industrial plains of Central Luzon, here is what is shaping the nation's real estate trajectory.

1. The Office Market: Quality Over Quantity

While the skyline continues to grow, the pace of office development has reached a steady, more calculated rhythm. Metro Manila is projected to add 350,000 square meters of new office space between 2026 and 2028.

Although these figures remain below pre-pandemic highs, leasing momentum is being sustained by a mix of outsourcing giants and traditional corporate firms.

The "Flight to Quality": Premium districts like Makati’s Ayala Avenue and Bonifacio Global City (BGC) remain the gold standard.

The Satellite Surge: Beyond the capital, Cebu, Pampanga, and Iloilo are cementing their status as vital business hubs, offering alternatives to the congested Metro.

2. Residential: The Rise of the 'Rent-to-Own'

The residential sector faces a unique challenge in 2026: moving 30,000 unsold, ready-for-occupancy (RFO) units across Metro Manila. To counter elevated mortgage rates, developers have moved away from traditional sales pitches in favor of flexible financial engineering.

"Developers are employing attractive promotions, extended payment terms, and rent-to-own schemes to capture mid-income buyers," Colliers noted in their report.

Demand is peaking in specific "lifestyle corridors," most notably the C5 Corridor and Katipunan. Proximity to prestigious universities and seamless connectivity to the Ortigas and Makati business districts have led some projects in these areas to reach 100% take-up.

3. Industrial: Central Luzon’s Dominance

In a massive geographic shift, Central Luzon has emerged as the country’s industrial powerhouse. The region is expected to deliver 870 hectares of industrial space through 2028—quadruple the pipeline of Southern Luzon.

This boom is fueled by the 99-year land lease law, a legislative shift that provides long-term security for foreign investors. This has positioned the Philippines as a competitive destination for high-growth sectors, including:

Semiconductor assembly

Automotive manufacturing

Renewable energy infrastructure

4. Retail: The Experience Economy

Brick-and-mortar retail is far from dead; it’s being reinvented. Retail vacancy rates are expected to dip below 10% by the end of the year, driven by a wave of mall refurbishments and the entry of new international brands.

Developers are no longer focusing solely on the capital. A "provincial push" is taking modern retail experiences to emerging urban centers like Bacolod and Davao, tapping into the rising purchasing power of regional consumers.

5. Hotels: Luxury and MICE Tourism

The hospitality sector is bracing for a busy year with 3,000 new hotel rooms slated for completion. Growth is concentrated in the Bay Area and Makati, bolstered by the presence of ultra-luxury brands such as Fairmont, Raffles, and OneKey Michelin-rated establishments.

Beyond leisure, the "MICE" segment—Meetings, Incentives, Conferences, and Exhibitions—is providing a steady stream of revenue as the Philippines re-establishes itself as a premier destination for regional business events.

Source: Data and insights based on the 2026 Property Market Outlook by Colliers Philippines.

#RealEstatePH #PhilippineRealEstateOutlook

Beyond the Skyline: 5 Trends Redefining Philippine Real Estate in 2026

MANILA, Philippines — The Philippine property landscape is undergoing a strategic transformation as 2026 begins, marked by a shift toward high-value corridors and aggressive developer incentives. According to the latest market outlook from Colliers, the industry is pivoting to meet a new era of consumer behavior and global investment interest.

Joey Bondoc, Director for Research at Colliers, identifies five critical sectors that are set to define the market this year. From the high-rise hubs of Metro Manila to the industrial plains of Central Luzon, here is what is shaping the nation's real estate trajectory.

1. The Office Market: Quality Over Quantity

While the skyline continues to grow, the pace of office development has reached a steady, more calculated rhythm. Metro Manila is projected to add 350,000 square meters of new office space between 2026 and 2028.

Although these figures remain below pre-pandemic highs, leasing momentum is being sustained by a mix of outsourcing giants and traditional corporate firms.

The "Flight to Quality": Premium districts like Makati’s Ayala Avenue and Bonifacio Global City (BGC) remain the gold standard.

The Satellite Surge: Beyond the capital, Cebu, Pampanga, and Iloilo are cementing their status as vital business hubs, offering alternatives to the congested Metro.

2. Residential: The Rise of the 'Rent-to-Own'

The residential sector faces a unique challenge in 2026: moving 30,000 unsold, ready-for-occupancy (RFO) units across Metro Manila. To counter elevated mortgage rates, developers have moved away from traditional sales pitches in favor of flexible financial engineering.

"Developers are employing attractive promotions, extended payment terms, and rent-to-own schemes to capture mid-income buyers," Colliers noted in their report.

Demand is peaking in specific "lifestyle corridors," most notably the C5 Corridor and Katipunan. Proximity to prestigious universities and seamless connectivity to the Ortigas and Makati business districts have led some projects in these areas to reach 100% take-up.

3. Industrial: Central Luzon’s Dominance

In a massive geographic shift, Central Luzon has emerged as the country’s industrial powerhouse. The region is expected to deliver 870 hectares of industrial space through 2028—quadruple the pipeline of Southern Luzon.

This boom is fueled by the 99-year land lease law, a legislative shift that provides long-term security for foreign investors. This has positioned the Philippines as a competitive destination for high-growth sectors, including:

Semiconductor assembly

Automotive manufacturing

Renewable energy infrastructure

4. Retail: The Experience Economy

Brick-and-mortar retail is far from dead; it’s being reinvented. Retail vacancy rates are expected to dip below 10% by the end of the year, driven by a wave of mall refurbishments and the entry of new international brands.

Developers are no longer focusing solely on the capital. A "provincial push" is taking modern retail experiences to emerging urban centers like Bacolod and Davao, tapping into the rising purchasing power of regional consumers.

5. Hotels: Luxury and MICE Tourism

The hospitality sector is bracing for a busy year with 3,000 new hotel rooms slated for completion. Growth is concentrated in the Bay Area and Makati, bolstered by the presence of ultra-luxury brands such as Fairmont, Raffles, and OneKey Michelin-rated establishments.

Beyond leisure, the "MICE" segment—Meetings, Incentives, Conferences, and Exhibitions—is providing a steady stream of revenue as the Philippines re-establishes itself as a premier destination for regional business events.

Source: Data and insights based on the 2026 Property Market Outlook by Colliers Philippines.

#RealEstatePH #PhilippineRealEstateOutlook